Buying a home is one of the most significant financial decisions most people make in their lifetime. One of the key questions that arise during this process is: what percent of your salary should your mortgage be? Understanding this helps you maintain a balanced budget, avoid overextending, and plan for future financial stability.

In this guide, we will explore recommended percentages, practical examples, factors that influence affordability, and strategies for managing mortgage payments responsibly.

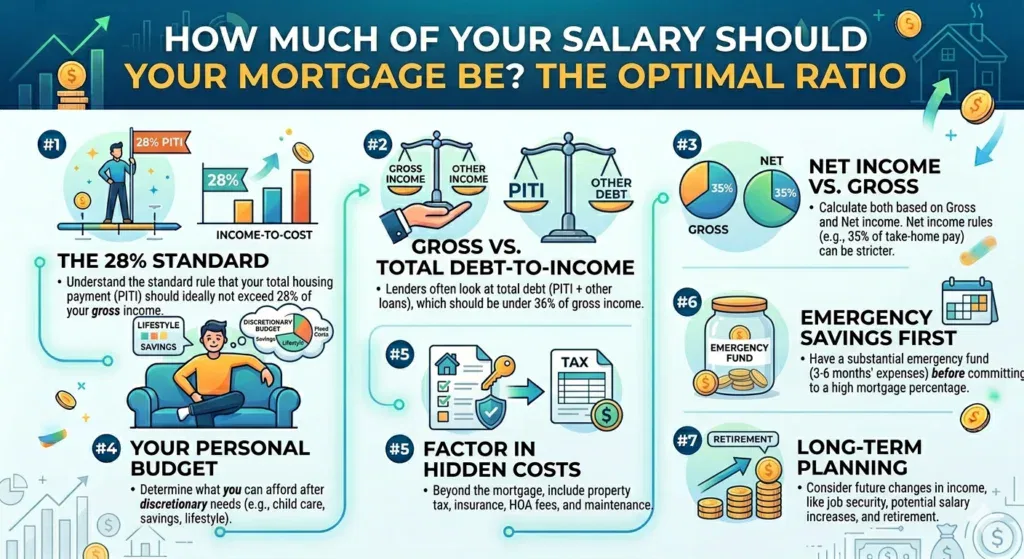

Why Knowing Your Mortgage Percentage Matters

Before diving into numbers, it’s important to understand why tracking your mortgage relative to your income is crucial:

- Financial Stability: Overspending on your mortgage can strain your finances, leaving little room for savings, emergencies, or investments.

- Affordability Planning: Knowing what percentage of your salary should your mortgage be helps set realistic expectations when house hunting.

- Debt-to-Income Ratio (DTI): Lenders often use this metric to evaluate how much of your income goes to debt, including your mortgage.

The goal is to find a balance: your mortgage should be large enough to meet your housing needs but not so large that it risks financial stress.

Step 1: The General Rule of Thumb

A widely accepted guideline is that your mortgage should not exceed 28% to 30% of your gross monthly income. Gross income refers to your total income before taxes and deductions.

Table 1: Mortgage Percentage Guidelines

| Income Level ($/month) | Recommended Mortgage Payment ($) | Percentage of Income (%) |

|---|---|---|

| 3,000 | 840–900 | 28–30 |

| 5,000 | 1,400–1,500 | 28–30 |

| 7,500 | 2,100–2,250 | 28–30 |

| 10,000 | 2,800–3,000 | 28–30 |

This range helps ensure you have sufficient cash for living expenses, savings, and unexpected costs.

Step 2: Consider Your Total Debt

While the 28–30% rule is helpful, it does not account for other debts. Lenders recommend a total debt-to-income ratio (DTI) of 36% to 43%, which includes:

- Car loans

- Student loans

- Credit card payments

- Other personal loans

Example: If your gross income is $5,000/month, your total monthly debt payments (including mortgage) should ideally be less than $1,800–$2,150.

Step 3: Adjust for Lifestyle and Expenses

Your mortgage percentage also depends on lifestyle and personal expenses:

- High Cost of Living Areas: You may need to allocate a slightly higher percentage to afford housing.

- Minimal Expenses: If you have few debts and low living costs, you can allocate a smaller percentage and save more.

- Family Needs: Larger families may require bigger homes, affecting the mortgage percentage of income.

Table 2: Adjusted Mortgage Percentage by Lifestyle

| Lifestyle Scenario | Recommended Mortgage % | Notes |

|---|---|---|

| Urban, high-cost city | 30–35% | May require higher allocation |

| Suburban, moderate expenses | 25–30% | Standard recommendation applies |

| Minimal debt & expenses | 20–25% | Opportunity to save more or invest |

Step 4: Include Taxes, Insurance, and PMI

Your mortgage payment often includes more than just principal and interest:

- Property Taxes: Varies by location, often 1–2% of home value annually.

- Homeowners Insurance: Typically $800–$1,500 annually.

- Private Mortgage Insurance (PMI): Required if your down payment is less than 20%.

Example: If your principal and interest payment is $1,200 and taxes, insurance, and PMI add $300, your total mortgage payment is $1,500.

This total should still fall within the recommended percentage of your salary.

Step 5: Calculate Mortgage Affordability Step by Step

- Determine your gross monthly income.

- Multiply by 28–30% to estimate your maximum mortgage payment.

- Subtract taxes, insurance, and PMI to find principal and interest affordability.

- Factor in other monthly debts to stay within a total DTI of 36–43%.

Table 3: Mortgage Calculation Example

| Step | Value ($) | Notes |

|---|---|---|

| Gross Monthly Income | 6,000 | Before taxes |

| 30% Allocation | 1,800 | Maximum recommended mortgage |

| Taxes, Insurance, PMI | 400 | Added monthly costs |

| Principal & Interest Affordability | 1,400 | Remaining for loan repayment |

Step 6: Impact of Interest Rates and Loan Terms

Interest rates and loan terms significantly influence what percent of your salary should your mortgage be:

- Higher Interest Rate: Increases monthly payments, reducing the affordable loan amount.

- Shorter Loan Term: Higher monthly payments, lower total interest.

- Longer Loan Term: Lower monthly payments, higher total interest.

Table 4: Monthly Payment by Interest Rate (Loan: $300,000)

| Interest Rate (%) | 15-Year Loan ($/month) | 30-Year Loan ($/month) |

|---|---|---|

| 4.0 | 2,219 | 1,432 |

| 5.0 | 2,370 | 1,610 |

| 6.0 | 2,531 | 1,799 |

Adjust your mortgage allocation based on current interest rates to stay within the recommended percentage.

Step 7: Strategies to Stay Within Your Mortgage Budget

- Increase Down Payment: Reduces loan amount and monthly payment.

- Refinance: Consider refinancing to a lower interest rate.

- Shorten or Lengthen Loan Term: Adjust payment amount while balancing total interest.

- Cut Expenses: Reducing discretionary spending increases affordability.

- Use Online Calculators: Simulate different scenarios to find a comfortable mortgage percentage.

FAQs About Mortgage Percentage

Q1: What percent of your salary should your mortgage be?

A: Generally 28–30% of your gross monthly income is recommended for principal and interest.

Q2: Can I spend more than 30% on my mortgage?

A: Yes, but it may strain your budget. Consider all other expenses and debts.

Q3: Does the mortgage percentage include taxes and insurance?

A: The 28–30% rule typically applies to principal and interest. Including taxes and insurance may increase the total percentage.

Q4: How does debt affect mortgage percentage?

A: Other debts are considered in the total DTI ratio, usually 36–43% of income.

Q5: Is 25% of salary on mortgage too low?

A: Not necessarily. It allows more flexibility for savings, investments, or lifestyle spending.

Q6: How do interest rates affect my mortgage percentage?

A: Higher interest rates increase monthly payments, requiring a smaller loan to stay within the same percentage.

Q7: Can I adjust mortgage percentage after buying a home?

A: Yes, through refinancing, extra payments, or extending loan term.

Q8: Should I consider mortgage insurance in my calculations?

A: Yes, if your down payment is below 20%, include PMI in your affordability calculations.

Q9: What is the safe DTI ratio for lenders?

A: 36–43% of gross monthly income, including all debts.

Q10: Does salary include bonuses for mortgage calculations?

A: Usually, lenders consider base income, but bonuses may count if consistent and documented.

Conclusion

Knowing what percent of your salary should your mortgage be is essential for financial health and stress-free homeownership. While the 28–30% rule is a helpful guideline, factors such as other debts, lifestyle, taxes, insurance, and interest rates play a major role in affordability. Using calculators, budgeting carefully, and adjusting your strategy based on your unique situation will help you stay within a comfortable range and avoid financial strain.

By following these seven smart guidelines, you can confidently determine a mortgage that aligns with your salary and long-term financial goals.